Regulation of the Mortgage Market Must Consider Shadow Banks

When we think about mortgages, what often comes to mind is a traditional bank or savings institution. The corner banker is seen as the mortgage lender and people get home loans at the same place where they may hold checking or savings accounts. But such a view does not reflect the real nature of the U.S. mortgage market. Mortgage lending in this country is highly segmented and traditional banks represent only an increasingly small part of the story. For many decades, banks have competed with independent mortgage companies that don’t take deposits and typically don’t have brick-and-mortar branches, a group that can be called “shadow banks.”

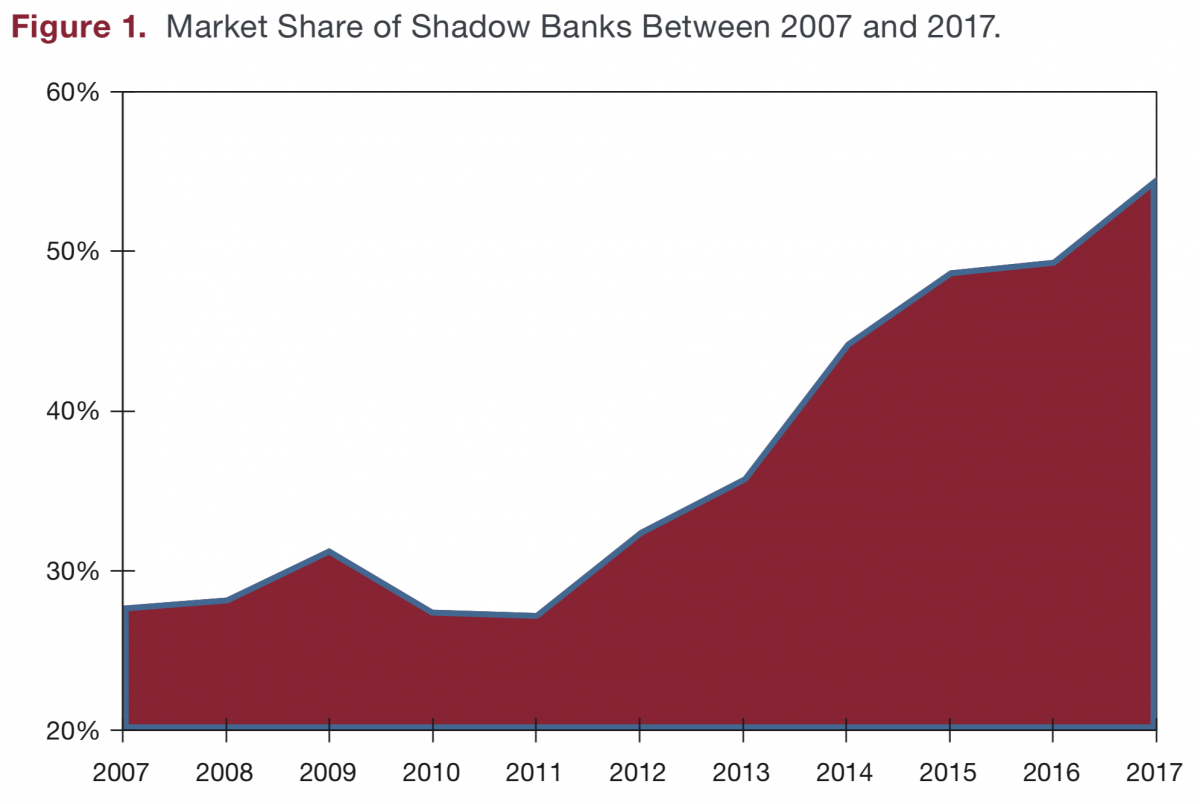

To understand the respective roles of traditional and shadow banks, Greg Buchak of the University of Chicago, Gregor Matvos of the University of Texas, Tomasz Piskorski of Columbia University, and I carried out a wide-ranging study of the mortgage market from 2007 to 2016, a period spanning the subprime mortgage crisis and housing crash, the Great Recession, the recovery of the housing market, and a long period of economic expansion (Buchak et al. 2018a). Analyzing mortgage application data and a range of other datasets, we documented the important presence of shadow banks over the past decade. Their presence has not been uniform during this period. Shadow banks had a major market presence before the housing crash of a decade ago, but then retreated amid widespread failures. Stunningly, since 2009, shadow banks have recovered their market share and now account for the bulk of new mortgage lending (see Figure 1).

In Buchak et al., (2018b), we find that the structure of the mortgage market, and in particular the rise of shadow banks, is a major factor determining the availability and price of home loans, and the safety and soundness of the banking system. For these reasons, public policies to regulate the U.S. mortgage market or encourage home ownership will be flawed unless they take into account the substantial market position of these nonbank lenders.

The U.S. Mortgage Market

U.S. residential mortgages constitute the world’s largest consumer finance market. More than 50 million residential properties currently have mortgages outstanding with a combined debt of about $10 trillion. The structure of this market is unique, reflecting the special role the federal government plays in promoting home loans. To make mortgages more widely available, Congress created Fannie Mae and Freddie Mac, private government-sponsored enterprises (GSEs) that buy home loans from lenders and package them as mortgage-backed securities (MBS) for sale to investors, guaranteeing payment if borrowers default.

By distributing loans to investors, the GSEs greatly expand the mortgage market, increasing the availability and lowering the price of mortgage credit. This market structure is one of the principal reasons why the U.S. homeownership rate is so high. However, the GSEs only buy loans up to a limit that has varied over time and by geography. Currently, that amount, called the conforming loan limit, is $453,100 for single-family homes in most parts of the country. Mortgages above that are classified as jumbo loans and are not eligible for purchase by the GSEs. Before the financial crisis, these loans could be sold to private investors, including investment banks such as Lehman Brothers. However, the market for selling these loans has evaporated since the crisis. Instead, jumbo mortgages are usually held by lenders on their balance sheets.

Traditional Banks and Shadow Banks

This structure is key to understanding the respective positions of traditional banks and shadow banks in the mortgage market. Traditional banks take deposits and use those funds to make loans, including mortgages. At the same time, they are heavily regulated and subject to strict requirements to hold capital against the loans they keep on their balance sheets. In the mortgage market, they have a choice: They can sell mortgages to the GSEs, collecting an origination fee and, in some cases, a fee for servicing the mortgages. Or they can hold mortgages on their balance sheets, collecting interest and principal until the loans are paid off, but taking the risk that borrowers will default. The better capitalized they are, the greater their capacity to keep mortgages. By contrast, shadow banks don’t take deposits and are lightly regulated. They generally don’t have the balance sheet capacity to keep the mortgages they originate. Their business model is originate-to-distribute, that is, to make mortgages and sell them to the GSEs.[1]

The differences in structure of traditional banks and shadow banks lead to two types of segmentation in the mortgage market. First, the stricter capital requirements and heavier regulatory burden traditional banks face put them at a competitive disadvantage in the conforming loan market. We show in Buchak et al. (2018a) that between 2008 and 2017, a period when bank capital requirements tightened, shadow banks grew their share of conforming mortgage originations from around 25 percent to almost 60 percent (see Figure 1). Because shadow banks are to a great extent locked out of the jumbo market, this increase in the market share of shadow banks is primarily confined to the GSE- sponsored conforming market, with traditional banks dominating on the jumbo side.

Second, we find that the balance sheet capacity to hold mortgages is an important factor explaining market segmentation because of differences among banks themselves. Banks that are flush with capital are more likely to hold mortgages on their balance sheets. Poorly capitalized banks are more likely to behave like shadow banks and sell the mortgages they originate. Thus, the market share of well-capitalized banks jumps 10 percent at the conforming loan limit.

To summarize, shadow banks have an advantage in the conforming mortgage market because they are lightly regulated. Traditional banks have an advantage in the jumbo market—a market in which it has been difficult to sell loans—because they take deposits and have the capacity to hold mortgages on their balance sheets. Well-capitalized banks are more likely to keep mortgages; poorly capitalized banks are more likely to act like shadow banks and sell mortgages on the secondary market.

|

Traditional Banks |

Shadow Banks |

|---|---|

|

Heavily Regulated |

Lightly Regulated |

|

Take Deposits |

Don't Take Deposits |

|

Can Hold Mortgages or Sell to GSEs |

Must Sell to GSEs |

|

Competitive Advantage in Jumbo Market |

Competitive Advantage in Conforming Market |

Policy Initiatives

This segmented market structure raises vital policy issues concerning the price and availability of mortgages, and the stability of the banking system. First, there are distributional effects. Policies that boost the availability of jumbo loans tend to benefit high-income borrowers, which would tend to raise levels of inequality; policies that increase the supply of conforming loans benefit less-affluent borrowers and would reduce inequality. Second are questions of systemic risk. Increasing the supply of jumbo mortgages mean a greater volume of mortgages held on bank balance sheets, which raises the level of credit risk in the banking system. But shifting mortgage supply to the conforming market creates additional credit risk for the GSEs. In 2008, Fannie Mae and Freddie Mac were found to be insolvent and were put into conservatorship, with the federal government assuming their obligations. Thus, a larger supply of conforming loans potentially raises the risk to the U.S. Treasury and, ultimately, to taxpayers.

Because of the interaction between shadow banks and traditional banks, and the segmentation of the market, an economic model of the U.S. mortgage market must allow for such linkages. The model built in Buchak et al. (2018b) permits an examination of how different policy initiatives might impact home loan volume and pricing, as well as distribution of benefits among borrowers and credit risk in the banking system. We examined three policy levers:

- Changes to capital requirements imposed on traditional banks

- Monetary policy initiatives to buy mortgage-backed securities, a policy known as quantitative easing when the Federal Reserve implemented it after the financial crisis

- Changes to the conforming loan limit

Changes to Bank Capital Requirements

Regulatory capital requirements imposed on banks increased from 4 percent in 2010 to 6 percent in 2015. We examined the effects of requirements at five levels between 3 percent and 12 percent. Our model shows that as capital requirements were progressively raised, banks shift from balance sheet lending to originate-to-distribute. Since selling of mortgages is only available for conforming loans, this change would shift origination from the jumbo to the conforming market and lower the share of mortgages held on bank balance sheets.

Notably, considering bank behavior alone would overstate the reduction in overall mortgage volume because tightening of capital requirements reduces the comparative advantage of traditional banks relative to shadow banks. As a result, lending activity would migrate from traditional banks to shadow banks. With a 9 percent capital requirement, we estimate jumbo interest rates would rise nine-tenths of a percentage point, jumbo lending would fall 40 percent, and bank portfolio mortgage holdings would drop 71 percent, hurting high-income borrowers. Since shadow banks would become more dominant, higher capital requirements would also move mortgage credit risk off bank balance sheets to the GSEs and indirectly to the U.S. Treasury.

Reducing capital requirements would have only modest effects on the volume of jumbo lending and interest rates. However, it could prompt a large increase in loans held on the bank balance sheets, raising risk in the traditional banking sector.

Monetary Policy

The Federal Reserve policy of buying mortgage-backed securities under a quantitative easing program tends to push down mortgage interest rates for loans sold to GSEs, raising conforming lending volumes significantly. For example, if quantitative easing were to trim MBS interest rates 0.25 percentage point, conforming loan rates would fall about the same amount. This would impact both traditional banks and shadow banks. However, because the GSEs don’t buy jumbo loans, interest rates in that market would not be affected. Focusing only on banks, which operate significantly on the jumbo side, would understate the true impact of the policy. The net effect would be a $165 billion increase in new conforming loans and little change in jumbo originations. Lower-income borrowers would feel the most impact because conforming loans would become more readily available and interest rates would fall. The jump in conforming loan volume would also shift credit risk to the GSEs.

Changes to Conforming Loan Limits

Before 2008, GSE conforming loans were capped at $417,000 for single-family homes, which limited lending in high-cost areas. To stimulate the housing market following the financial crisis, the limit was raised as high as $729,750. Currently, the conforming loan limit varies from $453,100 to $679,650.

We considered a range from a nationwide $417,000 cap to removing the limit altogether. Not surprisingly, raising the limit moves originations from the jumbo to the conforming market and lowers interest rates in both markets. The jumbo market would continue to exist because of other rules, including limits on loan size relative to property value. The prime beneficiaries of higher conforming loan limits would be high-income borrowers who would gain either because they would now be able to borrow in the conforming market or through lower rates in the jumbo market. Higher limits would have a muted effect on bank stability because well-capitalized banks would continue to keep a substantial share of conforming loans on their balance sheets. Since changes to the GSE- sponsored market impacts shadow banks substantially, focusing only on banks, which operate significantly on the jumbo side, would again understate the true impact of the policy.

Conclusion

Shadow banks now occupy a large and important part of the mortgage market. Their funding and operations differ starkly from those of traditional banks. We find that a complete analysis of the mortgage market must take into account the full range of lenders, including both traditional banks and shadow banks, and consider how policy initiatives would affect their relative market positions. In particular, policy actions could change the relative market shares of traditional and shadow banks, and affect the volume, cost, and distribution of both GSE conforming loans and jumbo loans. Broadly speaking, initiatives that raise the share and lower the cost of conforming loans benefit lower-income borrowers and shift credit risk to the GSEs, and by extension, to the U.S. Treasury. Focusing only on the banking sector would understate the impact of such policies because of the expansion of shadow banks. Policies that support the jumbo market offer gains to higher-income borrowers and shift risk to the banking system.

References

Buchak, G., G. Matvos, T. Piskorski, and A. Seru. (2018a) Fintech, Regulatory Arbitrage, and the Rise of Shadow Banks, Journal of Financial Economics, 130(3), 453-483.

Buchak,G., G.Matvos, T. Piskorski, and A. Seru. (2018b) The Limits of Shadow Banks (NBER Working Paper Series No. 25149) Cambridge, Mass.

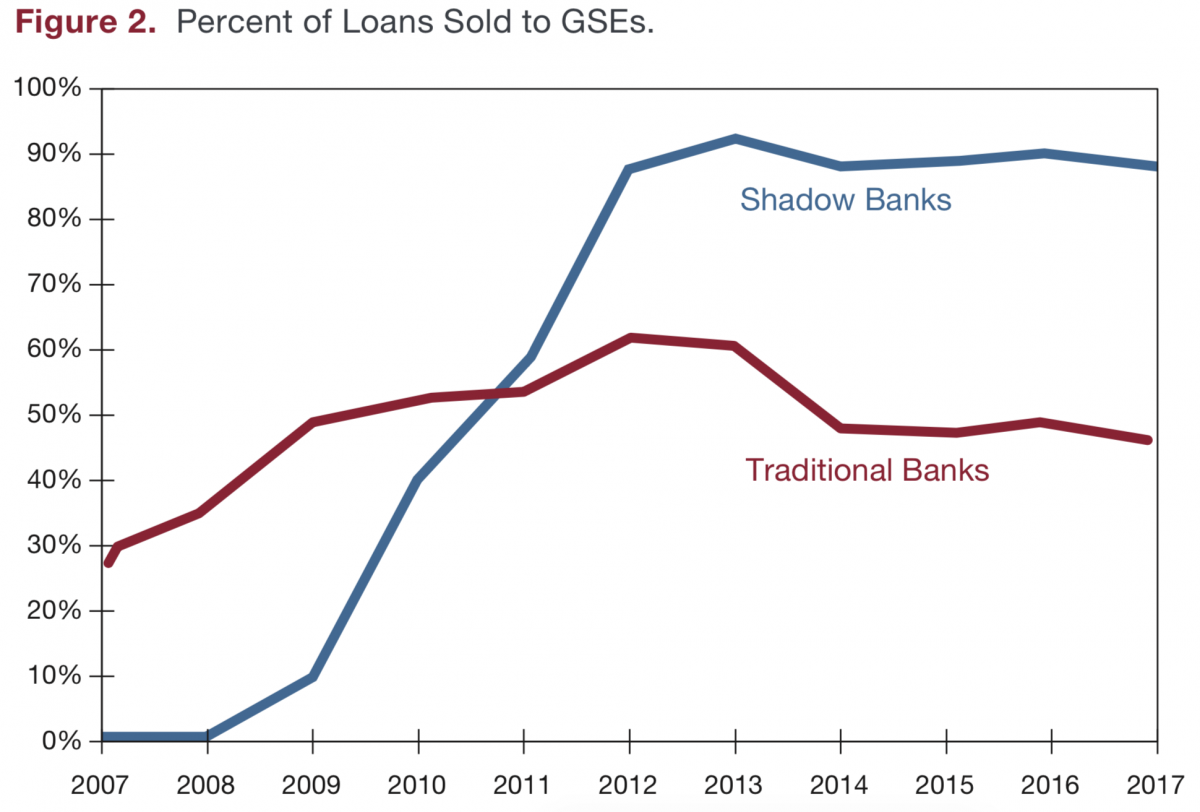

[1] An easy way to see this is to compare the loans sold to GSEs by traditional banks versus shadow banks. In Figure 2, one can see that shadow banks sell virtually all their loans to GSEs while traditional banks only partially do so.