Economic policy in a Biden administration

Key Takeaways

- The COVID-19 recession demands greater financial support for individuals, employers, and state and local governments.

- The 12 remaining states that have not yet adopted the ACA Medicaid expansion should do so as soon as possible.

- There’s an urgent need to save Medicare and Social Security before their trust funds go bankrupt in 2024 and 2032, respectively.

- Massive and rising federal deficits coupled with soaring income and wealth inequality make clear that the time is now for targeted tax reform.

- A carbon tax coupled with programs to help low- and middle-income workers will strengthen our environment and our economy for the long term.

When Joe Biden takes the oath of office as the country’s 46th president on Jan. 20, 2021, the country will be at a very different place from when he launched his campaign on April 25, 2019. The unemployment rate will be approximately twice as high and the federal deficit will have ballooned.

More than 15 million Americans will have contracted COVID-19 during 2020 and the total number of deaths from this illness will likely exceed 300,000. This will make the virus the third-leading cause of death in 2020 (behind heart disease and cancer) and will exceed the sum of all deaths from all accidents, suicides, homicides, influenza, and pneumonia.

Tens of millions of our nation’s K-12 and post-secondary students will have been forced to learn remotely while tens of millions more people will be working from home. These changes to our health and economic well-being have differentially hit women and minority groups (Bureau of Labor Statistics, 2020)1 and have surely contributed to the 28 percent increase in the nation’s homicide rate this year relative to just one year ago (Jackman, 2020).

Taken together, all of this would present a gigantic challenge to any new administration at any time in our nation’s history. This challenge will almost surely be made more difficult by the bitter partisanship that has gripped the country during the past year. Democrats will next year have just a 51 percent majority in the House. And — depending on Georgia’s two special elections in January — can hope for no better than a 50-50 split in the Senate.

In this policy brief, I outline several policy proposals for a Biden administration to pursue in response to the challenges posed by COVID-19 along with the current and projected economic situation. This list is not meant to be exhaustive and focuses primarily on government expenditure programs and tax policy.

Bolster unemployment benefits and help state and local governments

While the unemployment rate has fallen steadily since reaching a high of 14.7 percent in May, workers in many industries — particularly leisure and hospitality — are still very hard-hit. This explains why Hawaii and Nevada have the highest unemployment rates.2

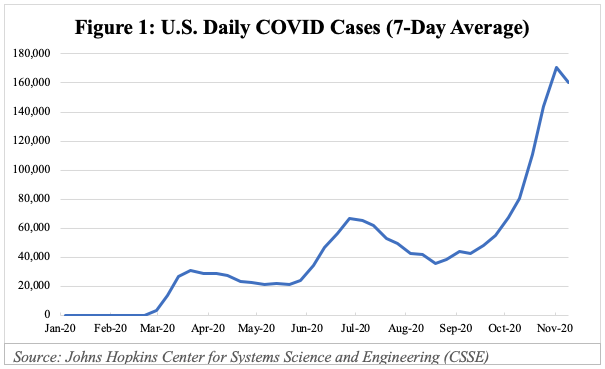

Any large-scale return to work will almost surely be stalled by the third wave of COVID-19 cases displayed in Figure 1, with the late-November peak about twice as high as the summertime peak.

Unemployment Insurance (UI) benefits are set to run out for millions of workers later this month and the number of workers newly claiming UI each week is still higher than at any point during the Great Recession. Without additional federal relief, many families will struggle and default on housing, student, and car loans. Credit card bills will go unpaid, along with rents and health care bills.

In different times, many economists would worry that more generous or longer-term unemployment benefits would discourage laid-off workers from finding new jobs. But these are not ordinary times and there is little evidence to suggest that the enhanced UI benefits paid during the pandemic discouraged workers from job hunting (Altonji et al., 2020).

The Biden administration should also prioritize giving financial assistance to employers. When a company lays off workers, it’s hit with a tax increase soon after, which is meant to offset the state’s unemployment insurance costs.

These tax increases could deter some firms from hiring or force them out of business. That would slow a recovery and require additional tax increases on surviving businesses — many of which are already on the financial edge. Providing targeted relief to employers to weather these and related challenges — as some soon-to-expire provisions of the federal CARES Act do — would give them a strong incentive to retain their workers or to expand operations rather than downsize or close.

State and local government budgets are also in crisis. Recent estimates suggest that the budget hit to state and local governments will be $240 billion in the current (2021) fiscal year and will be even greater in 2022 (Clemens and Veuger, 2020).

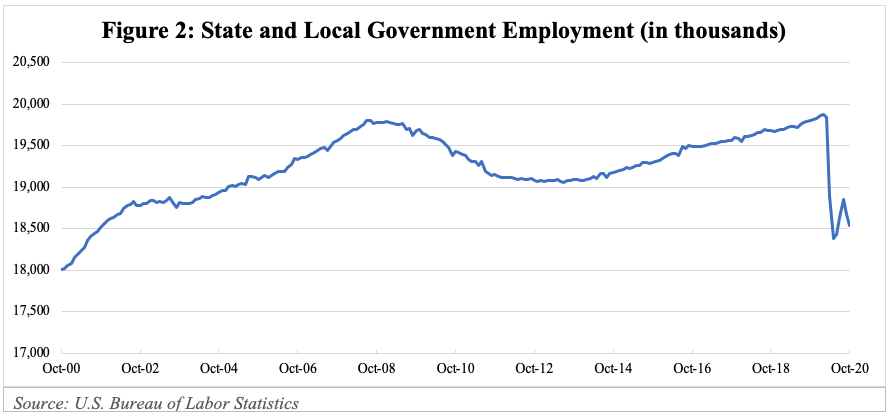

Absent substantial aid from the federal government, these financing challenges will result in significant cuts to government services including education, health care, and criminal justice. And those cuts mean government worker layoffs. As shown in Figure 2, state and local government employment already dropped from 19.9 million in February to 18.5 million in October. This contrasts with the private sector, where employment numbers tanked in the first few months of the pandemic but have recently been climbing back.

The loss of public employees is particularly troubling at a time when the pandemic is putting more demands on government agencies and institutions like schools and hospitals. Research has shown that federal aid to state and local governments during the Great Recession cushioned the economic damage and stimulated employment increases (Chodorow-Reich et al., 2012). This support likely also translated into fewer cuts to education and health care, with these investments paying dividends far into the future in the form of higher earnings and better health.

Given that evidence, the Biden administration should be confident in moving ahead with substantial aid to cushion the pandemic’s economic shock.

Improve health care and expand insurance coverage

The pandemic has put unprecedented strain on the health care system. Employment in the sector dropped 10 percent in March and April with the loss of 1.6 million jobs.3 More than half of this decline has been made up during the past several months due in part to the significant financial stimulus provided by the federal CARES Act in the spring.

But recovery has slowed, and health care employment is still about 4 percent (590,000 jobs) lower than at its February 2020 peak. This is all the more concerning given that COVID-related demands on our health care system are surging, with hospitalizations and new daily cases much higher in the past month than at any time during the pandemic.

The COVID-induced declines in employment in all sectors have also taken a toll on health insurance coverage among workers and their families, with recent research estimating that 7.3 million people lost employer-based health insurance along with their jobs (Banthin et al., 2020). But estimates of the overall reduction in coverage were much lower at just 2.8 million, primarily because the federal-state Medicaid program provided a “safety net” with enrollment in this program rising by 4.2 million people over the same period. This coverage allowed workers and their families to retain access to health care while covering the costs of most of their medical expenses.

That is a testament to the 2010 Affordable Care Act (ACA), which allowed states to expand their Medicaid programs so that low-income residents without insurance could have 90 percent of their health care costs covered by the federal government (with the remaining 10 percent covered by states).

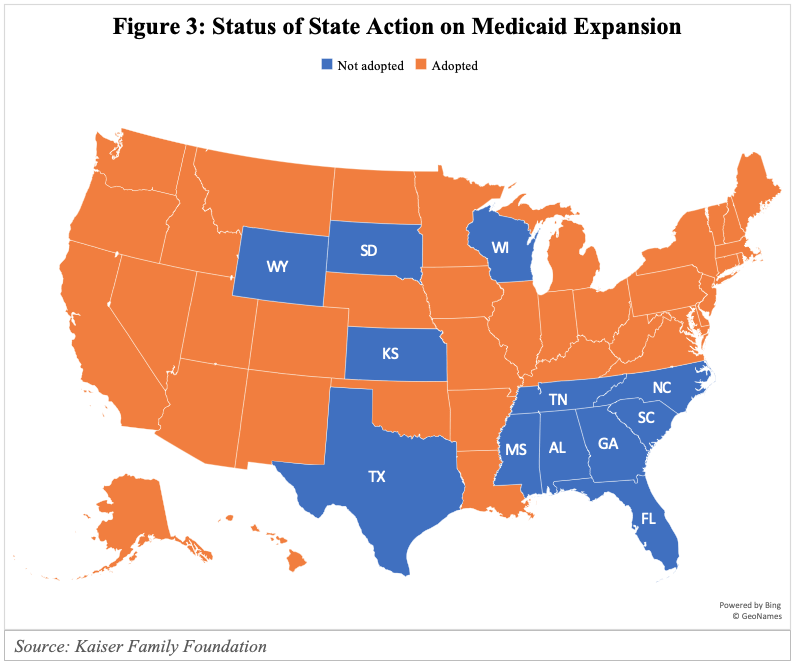

The law significantly expanded health insurance coverage (Duggan, Goda, and Jackson, 2019) and helped to slow the growth in health care costs4. Perhaps even more important, recent research has shown that health outcomes improved significantly more in states that decided to expand Medicaid soon after ACA passage (Johnson et al., 2020). But a 2012 Supreme Court decision allowed states to opt out of the expansion, and 12 states have still refused to add the coverage (see Figure 3).

As of 2019, only 7 percent of residents in states that expanded Medicaid were still without health insurance. The corresponding share in the dozen states that haven’t expanded was almost twice as high at 13 percent (Keisler-Starkey and Bunch, 2020).

The Biden administration should encourage policymakers in these 12 states — which include several swing states such as Florida, Georgia, North Carolina, and Wisconsin — to expand their Medicaid programs. This will strengthen the health care delivery systems in these states and improve the health and economic well-being of the millions of residents who will gain insurance.

In addition to expanding Medicaid, the ACA also provided subsidies for individuals with incomes too high to qualify for Medicaid to purchase private health insurance coverage through ACA insurance exchanges. Coverage in the exchanges rose between 2014 and 2016, but has declined in every year since (Kaiser Family Foundation, 2020). A key contributor to this four-year decline has been that the federal government has shortened the coverage enrollment window from 12 weeks to 6 weeks, while also cutting resources to consumer outreach.

Reversing these recent policy changes could substantially increase the number of Americans with health insurance coverage. It’s an inexpensive investment with a substantial return, and the Biden administration should make the move so that more Americans have the affordable health insurance coverage for which they are eligible. Reforms that expand subsidies to coverage in the ACA exchanges or that introduce a public option into these exchanges could lead to still further reductions in the number of Americans without health insurance.

The U.S. also needs to be better prepared for future health crises. We have learned a tremendous amount during this pandemic about equipping our front-line workers, incentivizing drug companies to develop therapeutics and vaccines, and how to test and track cases so we can more rapidly contain outbreaks. Applying these lessons through additional funding for critical agencies such as the CDC (whose $8 billion budget represents less than 0.2 percent of the overall federal budget) will allow us to more aggressively and efficiently confront any similar future health threats and will better protect us against economic catastrophe.

Protect Medicare

The trust fund of Medicare Part A — which primarily covers inpatient hospital expenses, hospice care, skilled nursing facilities, and home health care for 65 million elderly and disabled Americans — is projected to go bankrupt in the next few years.5

The annual report produced by the Board of Trustees of the Medicare program earlier this year showed that this trust fund would reach zero in 2026 following a steady decline during the past 12 years —thanks primarily to an aging population and a declining ratio of workers (who finance the program through their payroll taxes) to Medicare recipients (Board of Trustees, 2020). These projections did not incorporate the economic effects of the COVID pandemic, and a more recent estimate by the Congressional Budget Office is even more dire: The CBO’s September report puts the trust fund at zero in 2024, just before the next presidential election (CBO, 2020a).

If the trust fund runs out of money, spending would need to be cut so that Medicare Part A expenditures did not exceed the program’s revenues. The consequences of such a change could be catastrophic for health care providers and for America’s 65 million Medicare recipients. If the incoming administration and Congress don’t fix this shortfall, there will be a new kind of health care crisis.

At a high level there are two types of fixes — raise taxes or reduce benefits.

On the tax front, policymakers could increase the Medicare tax rate on earnings from its current 2.9 percent, which is paid on all earnings (and split evenly by employers and employees). An additional tax of 0.9 percent is levied (on employees) for all earnings in excess of $200,000 annually ($250,000 for married couples). Policymakers could increase one or both tax rates or introduce a third tax bracket for even higher levels of income (e.g., $400,000 and above).

The revenue gains from even just a 1 percentage point increase in the 2.9 percent rate would be substantial, with estimates by CBO suggesting almost $100 billion annually from this measure (CBO, 2018). Such a change would extend the solvency of the Medicare trust fund for a decade or more. The distributional effects of this would however be regressive, since low-income workers derive a larger share of their income from earnings (capital gains and other sources of investment income are not currently subject to the Medicare payroll tax). Comparable increases in the 0.9 percent rate on high-income earners would generate much less in revenues but would insulate low- and middle-income workers from the tax increase.

Tackle the federal debt

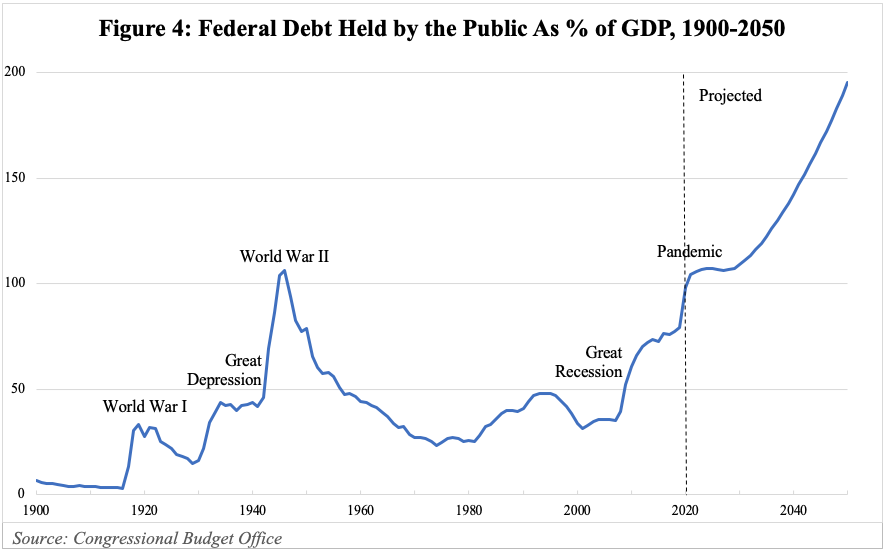

The federal debt is one of the greatest challenges for policymakers in the years ahead. Even before the pandemic’s onslaught in March, the CBO projected a steadily rising deficit, with expenditures projected to be 23.4 percent of GDP in 2030 versus revenues of just 18.0 percent of GDP in that same year (CBO, 2020b). The agency further projected that federal debt “held by the public” would reach 98 percent of GDP in that year, which would be the highest in the post-World War II era.

The pandemic made things much worse, much faster. The federal debt reached 100 percent of GDP this year — 10 years sooner than the CBO predicted in January.

Our federal debt is now projected to double as a share of GDP over the next 30 years, reaching 200 percent of GDP by 2050 (CBO, 2020c). And this projection is arguably optimistic, as it factors an increase of tax revenue expected with the expiration of President Trump’s Tax Cuts and Jobs Act in 2025.

While the cost of this federal debt burden is cushioned by historically low interest rates, it seems plausible that interest rates will increase in the not-too-distant future, further straining the federal budget. Consistent with this, the CBO expects interest on the federal debt to more than quadruple as a share of GDP between 2030 and 2050. And even with the current low interest rates, interest payments for the federal debt totaled about $380 billion in the 2020 fiscal year (CBO, 2020b).

To put this figure in context, it is equivalent to about 6 months of total spending for the Medicare program described above.

Push for targeted tax increases and reform

There are two big levers policymakers can pull to reduce the federal deficit — raise taxes or lower spending. Of course, an increase in economic growth — along with the associated increase in individual and corporate income — can also lower the deficit, and so it is important to craft policy with this outcome in mind.

There are a number of proposals to increase taxes — from raising capital gains taxes and income tax rates of the richest Americans, to hiking the corporate income tax rate. Each policy prescription delivers some immediate pain, though the long-run benefits of lowering the deficit would be substantial.

Recent data on income and wealth accumulation in the U.S. suggest that inequality has been steadily increasing for the last four decades (U.S. Census Bureau, 2020; Federal Reserve Board, 2020).

One commonly used measure of inequality is the ratio of income among those at the 90th percentile of the income distribution to income at the 10th percentile. As shown in Table 1, this 90-10 ratio increased from 9.1 in 1980 to 10.6 in 2000 and then to 12.6 by 2018. And there is clearly no sign of a slowdown in this measure after the Great Recession, as the annual increase from 2010 to 2018 was identical to the corresponding rise from 2000 to 2010.

Wealth inequality has also increased significantly over this period, with the ratio of average wealth among the top 10 percent of the population to average wealth among the other 90 percent rising from 14.7 in 1989 to 22.0 by 2019. This increase was almost entirely driven by gains among the top 1 percent of the population. Average per-capita wealth for this group is now 102.4 times greater than average wealth among the lower 90 percent (versus just 62.0 times greater 30 years ago).

While these growing disparities have been driven partly by rising earnings inequality, they also reflect the strong performance of the stock market and other sources of investment income. Income from dividends and capital gains accounts for a much larger share of income among high earners.

The current capital gains tax starts at 15 percent for those with annual incomes from $80,000 to $440,000 and then increases to 20 percent for those with incomes beyond $440,000 (there is an additional 3.8 percent net investment income tax for high earners). These tax rates are substantially lower than the corresponding rates on ordinary income, which led to Warren Buffett’s lament that his marginal tax rate was lower than his secretary’s6.

Recent CBO projections indicate that a two percentage point increase in these two capital gains tax rates would generate more than $7 billion in revenue annually (CBO, 2018). Clearly, this one change would not solve the budget difficulties highlighted above but would make a large dent.

Another possible source of revenue that would not affect the vast majority of taxpayers but could generate significant revenues would be an increase in the marginal tax rate on ordinary incomes. At present, those filing jointly pay a tax rate of 35 percent on all income between $415,000 and $623,000 and a tax rate of 37 percent on income above $623,000.

According to CBO projections, an increase of just one percentage point in these two tax rates would generate an average of $12 billion to $14 billion annually over the next decade (CBO, 2018). Raising each of these rates by 2.6 percentage points (so that the top rate would return to 39.6 percent, where it was during 1993 – 2000 and 2013 – 2017) would generate about $33 billion in annual revenue and put the country on a much better economic trajectory.

Corporate taxes also need to be addressed. The 2017 Tax Cuts and Jobs Act lowered the tax rate on most corporate income from 35 percent to 21 percent (an average of 25.9 percent when state taxes are included). Prior to this change, the U.S. rate was substantially higher than in most industrialized countries. The current rate is now lower than in all other G-7 nations except the U.K., which has a corporate tax rate of 19 percent (Tax Policy Center, 2020).

While the U.S. now has a lower tax rate than most other industrialized countries, according to data from the OECD’s Tax Revenue Statistics, we are a much bigger outlier with respect to corporate tax revenues as a share of GDP. In the U.S., corporate income tax payments represent just 1.1 percent of GDP versus 2.1 percent in Germany, 2.9 percent in the U.K. (despite its lower tax rate), and 3.7 percent in Canada (Tax Policy Center, 2020). This is especially surprising — as U.S. corporations are arguably the most profitable in the world — and primarily reflects our relatively narrow tax base.

The Biden administration should push for reduced deductions and exclusions from corporations’ taxable income and thereby broaden the tax base. An alternative would be to increase corporate income tax rates, with the CBO estimating that each 1 percentage point increase generates about $8 billion in revenues annually (CBO, 2020a).

At a minimum, policymakers should take the relatively uncontroversial approach of increasing resources for the IRS to better enforce tax codes. Estimates from 2011 to 2013 suggest that 16 percent of the federal taxes that were owed each year were ultimately not paid. The magnitude of “missing federal taxes,” which averaged about $380 billion annually7 during the three-year period, has almost surely increased, given that from 2010 to 2020 appropriations for the IRS fell by 22 percent in inflation-adjusted terms and the agency consequently reduced its staff by 20 percent. Even more striking, the share of individual income taxes that were audited fell by almost half (46 percent) and the corresponding share of corporations that were audited fell by 37 percent (CBO, 2020d).

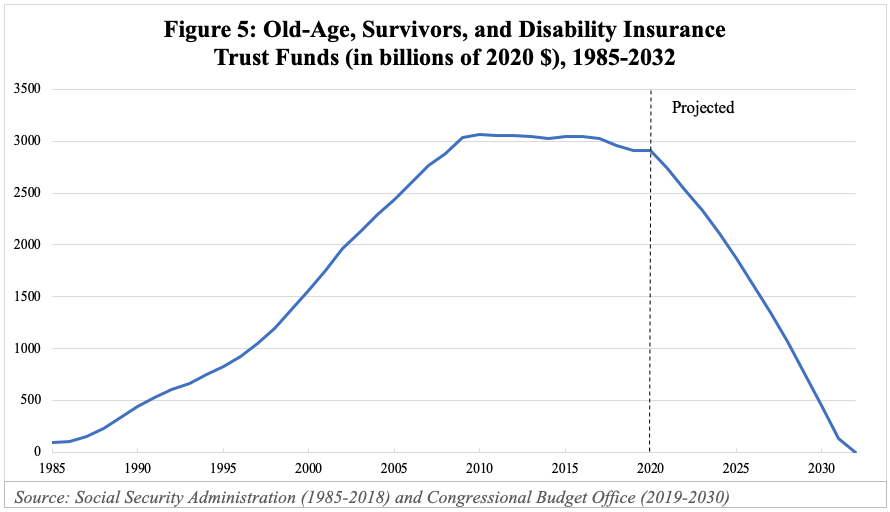

Save Social Security

Social Security is the U.S.’s largest government program. It paid an average monthly benefit of $1,400 to 65 million Americans in October 2020 (SSA, 2020a). The 46 million retirees drawing the benefit represent the largest group of Social Security recipients, but the program also covers 8 million disabled workers, 6 million survivors (primarily widows), and 5 million dependents. The program represents the majority of income for most elderly Americans and provides a crucial safety net for millions of individuals with disabilities.

Social Security (also known as OASDI for Old Age, Survivors, and Disability Insurance) operates largely on a pay-as-you-go basis, with current payroll taxes financing nearly 90 percent of current benefits. However, during the past 35 years, the program has gradually built up a trust fund that — at the end of the 2019 calendar year — stood at $2.9 trillion (SSA, 2020b). The trust fund is invested entirely in U.S. Treasury securities and is not counted in the federal debt “held by the public.”

It does, however, represent a very real obligation of the federal government. The growth in the OASDI trust fund has been slowed by the reduction in interest rates described above, with its interest income falling from $118 billion in 2009 to just $81 billion in 2019 despite a $360 billion rise in the fund’s balance during that same period.

The Social Security program will almost surely run a deficit in 2020 for the first time since 1981, when the program did not have a meaningful trust fund and was on the brink of insolvency. At that time, President Reagan worked closely with House Speaker Tip O’Neill to forge a bipartisan compromise that extended the program’s solvency for several decades into the future.

The 1983 Social Security Amendments involved an even mix of tax increases and benefit reductions that allowed the program to run surpluses and accumulate a significant trust fund in anticipation of the demographic challenge caused by the aging of the baby-boom generation.

As was expected then, the OASDI trust fund has started to decline as shown in Figure 5. This looming shortfall has been understood and is largely driven by the aging of the baby-boom generation into retirement years, increases in life expectancy, and the corresponding reduction in the number of workers per retiree.

Previous Democratic and Republican administrations have tried tackling the funding challenges of Social Security and other entitlement programs. But no significant reforms have been made to improve their long-run solvency in almost four decades.

Given the political challenges of either raising taxes or reducing benefits, one could reasonably ask why the Biden administration should tackle the issue. But if it doesn’t, Social Security will be flat broke in about a decade. That would mean an automatic, across-the-board cut in benefits and the imposition of unacceptable financial burdens on our country’s Social Security recipients. And there will be about 80 million of them when this happens.

To strengthen this program, it is important to get Social Security on a stronger financial footing as soon as possible. On the revenue side, the two primary levers are the 12.4 percent payroll tax rate and the $137,700 tax base for the program (which is scaled up annually with average wage growth).

According to CBO estimates, a one percentage point increase in the payroll tax rate would extend the program’s solvency by another four years through the additional tax revenue that it would generate (CBO, 2018). Raising the tax rate by two percentage points would extend the date of trust fund exhaustion by about nine years. One limitation to this approach is that it would differentially hit lower- and middle-income workers, who derive most of their income from earnings and do not have earnings high enough to avoid the OASDI payroll tax.

An arguably even more attractive option would be to increase the tax base for OASDI benefits. At the time of the 1983 reforms, approximately 90 percent of all earnings were subject to the program’s payroll tax. However, because earnings have grown much more rapidly for high earners than for the rest of America’s workers, the share of earnings covered by the OASDI payroll tax has fallen to just 83 percent (CBO, 2018).

If this tax base was adjusted to once again cover 90 percent of all earnings, this would more than double the tax base to about $295,000 and extend the program’s solvency by another five years. These two changes make clear that — as was true in 1983 — it will be very difficult to fix Social Security through tax increases alone.

On the benefit side, perhaps the most obvious option would be to once again increase the program’s full retirement age (FRA). The main disadvantage of such an approach is that it would differentially hit lower- and middle-income workers, who have much shorter life expectancies than their high-income counterparts. And this inequality in life expectancy has increased significantly in recent years (Isaacs and Choudhury, 2017).

An alternative reform would revise the Social Security benefit formula so that benefits are reduced only for higher-income workers. A carefully crafted change of this type — along with an expansion of the payroll tax base — could extend Social Security’s solvency for many years into the future.

Help workers while tackling climate change

A number of ideas to increase employment and improve economic well-being among low- and middle-income workers are undoubtedly on the horizon. Ideally, these provisions would be “paid for” with additional revenues so as not to exacerbate the federal budget difficulties described above.

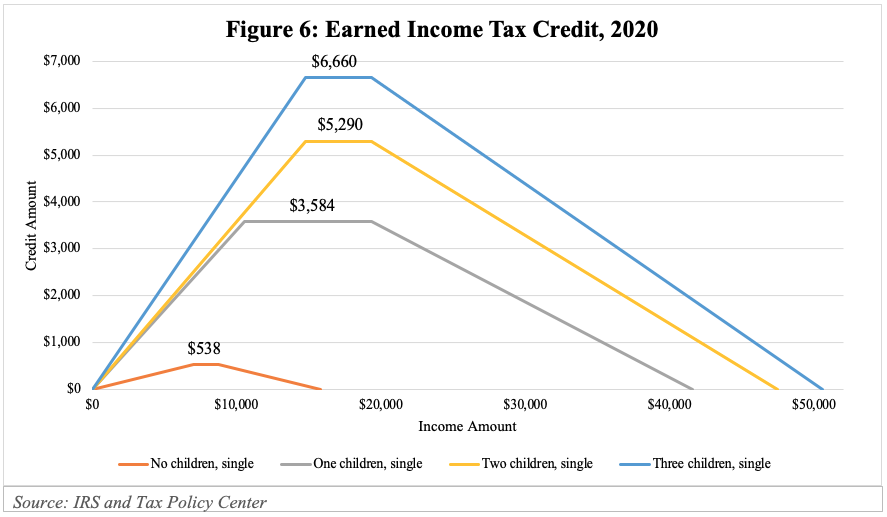

One provision of the tax code that has been very successful in increasing employment and increasing workers’ take-home pay is the earned income tax credit (EITC). As Figure 6 shows, the EITC substantially increases the return-to-work for many individuals through a wage subsidy. For example, a full-time worker with two children who earns $9 per hour (about $19 thousand annually) would receive a $5,800 tax subsidy through the EITC. That effectively raises the worker’s hourly wage to about $12. However, as this same figure shows, this subsidy is significant only for workers with children, as those without children with similar earnings currently receive just a modest EITC subsidy.

One straightforward policy change that would have a high bang-for-the-buck would be to expand the EITC for adults without children. In contrast to the EITC for adults with children, the tax credit for childless adults has barely changed since the early 1990s. An important benefit of this policy is that it would raise employment among lower-income workers and would therefore to some extent “pay for itself.” Recent estimates suggest that tripling the maximum EITC benefit for adults without children (from about $500 to $1500) would increase the credit paid to about 8 million workers while making an additional 16 million workers eligible for the EITC (Maag et al., 2019).

This is just one example of a federal policy lever that could substantially improve economic well-being among lower- and middle-income workers in the U.S. Expanding the EITC and similar interventions on this front would entail some budgetary cost.

While any tax increase to pay for an expanded EITC or other interventions to help lower- and middle-income families would impose some financial burden, quite possibly the most economically efficient change on this front would be to introduce a carbon tax.

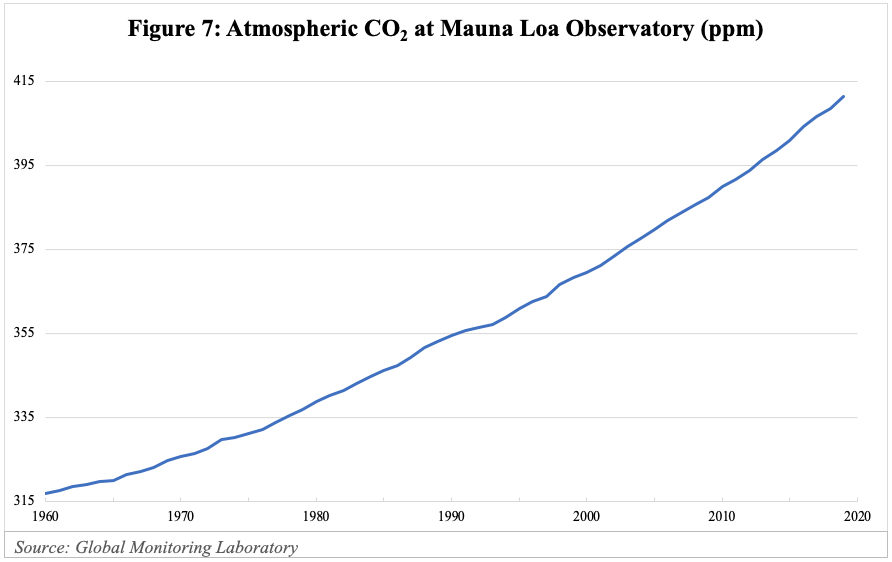

This would give individuals and companies a strong financial incentive to shift from carbon-intensive technologies to those that are more energy-efficient or that use renewable energies. The resulting reduction in CO2 emissions could help to slow the steady increase in the atmospheric concentration of CO2 shown in Figure 7, which is contributing to climate change including more frequent hurricanes, wildfires, and higher temperatures that adversely affect human health and economic well-being.

Economists tend to support a carbon tax, as it allows market forces to shift resources to efficiently reduce greenhouse gas emissions, which impose significant health and economic costs on a large segment of our population (Greenstone et al., 2013).

Relative to other countries, our tax on gasoline and other sources of CO2 are very small. For example in the U.S. the federal gasoline tax is 18.4 cents per gallon with an additional 34 cents per gallon for the average state and local tax. Our overall tax of 52 cents per gallon is much lower than in other countries, such as Canada ($0.74), Australia ($1.15), Germany ($2.79), and the U.K. ($2.82), with the overall OECD average at $2.24 (Watson, 2019).

According to CBO estimates, a tax on greenhouse gas emissions of $25 per metric ton would generate more than $100 billion annually in additional revenue (CBO, 2018), which would be more than sufficient to fund a substantial expansion of the EITC and other government programs to help workers and families, while still making a substantial dent in the federal deficit going forward. This tax could be bundled with additional provisions to reduce any adverse distributional consequences.

Conclusion

The economic problems facing the incoming administration and newly seated Congress are many. And they are complex. But assisting individuals, employers, and state and local governments is their most urgent priority.

Many of the proposals that I have outlined require sacrifices. Failing to make them will put two of our country’s largest and most cherished programs at risk, while saddling our children and grandchildren with unprecedented amounts of federal debt.

It’s true that interest rates are low and the federal government can borrow money cheaply. But there’s no guarantee on tomorrow, and those interest rates could increase the expense of taking on even more debt. The risk of massive further increases in borrowing isn’t worth it.

My proposals focus primarily on raising revenues in a targeted way with a recognition that both income and wealth inequality in the U.S. has soared over the last 40 years. One could alternatively propose a plan that cuts spending to achieve the same amount of deficit reduction. If that path prevails, policymakers must use extreme caution to protect the most vulnerable Americans from cuts to benefits and services that are — in many cases — a true lifeline.

Given the rising polarization in the U.S. and the likely divided government, one could be pessimistic about the prospects of political compromise and cooperation. But I am optimistic that the Biden administration and Congress will rise to the challenge of securing a brighter future for America.

Footnotes

1 From the third quarter of 2019 to the third quarter of 2020, the unemployment rate increased 14 percent more among women than men, by 69 percent more among black than white individuals, and by 56 percent more among Hispanic than white individuals. Data accessed 11/30/2020: https://www.bls.gov/web/empsit/cpsee_e16.htm.

2 In October 2020, Hawaii’s and Nevada’s unemployment rates were 14.3 and 12.0 percent, respectively. Data accessed 11/30/2020: https://www.bls.gov/web/laus/laumstrk.htm.

3 Bureau of Labor Statistics data accessed 11/30/2020: https://fred.stlouisfed.org/series/CES6562000101.

4 Health care spending as a share of GDP increased from 13.3% in 2000 to 17.4% in 2009 but then rose to just 17.8% in 2018. Data accessed 11/30/2020: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical.

5 Medicare Part B covers physician and outpatient services while Medicare Part D covers prescription drugs.

6 See https://money.cnn.com/2013/03/04/news/economy/buffett-secretary-taxes/index.html.

7 IRS estimates that an average of $441 billion was unpaid annually but that an average of $60 billion annually was captured through audits and other enforcement efforts.

References

Altonji, Joe, et al. “Employment Effects of Unemployment Insurance Generosity during the Pandemic.” Yale University mimeo. 2020.

Banthin, Jessica, Michael Simpson, Matthew Buettgens, Linda Blumberg, and Robin Wang. “Changes in Health Insurance Coverage due to the COVID-19 Recession.” Robert Wood Johnson Foundation and Urban Institute. July 2020.

Board of Trustees Federal HI and Federal SMI Trust Funds. 2020 Annual Report of the Board of Trustees of the Federal Health Insurance and Federal Supplemental Medical Insurance Trust Funds. April 2020.

Chodorow-Reich, Gabriel, Laura Feiveson, Zachary Liscow, and William Gui Woolston. “Does State Fiscal Relief during Recessions Increase Employment? Evidence from the American Recovery and Reinvestment Act.” American Economic Journal: Economic Policy. August 2012. Pages 118-145.

Clemens, Jeffrey, and Stan Veuger. “The COVID-19 Pandemic and the Revenues of State and Local Governments: An Update.” AEI Economic Perspectives. September 2020.

Congressional Budget Office. “Options for Reducing the Deficit: 2019 to 2028.” December 2018.

Congressional Budget Office. 2020a. “The Outlook for Major Federal Trust Funds.” September 2020.

Congressional Budget Office. 2020b. “The Budget and Economic Outlook: 2020 to 2030.” January 2020.

Congressional Budget Office. 2020c. “The 2020 Long-Term Budget Outlook.” September 2020.

Congressional Budget Office. 2020d. “Trends in the Internal Revenue Service’s Funding and Enforcement.” June 2020.

Duggan, Mark, Gopi Shah Goda, and Emilie Jackson. “The Effects of the Affordable Care Act on Health Insurance Coverage and Labor Market Outcomes.” National Tax Journal. 2019. Pages 261-322.

Federal Reserve Board of Governors. “Wealth and Income Concentration in the SCF: 1989-2019.” September 2020.

Greenstone, Michael, Elizabeth Kopits, and Ann Wolverton. “Developing a Social Cost of Carbon for U.S. Regulatory Analysis: A Methodology and Interpretation.” Review of Environmental Economics and Policy. 2013. Pages 23-46.

Isaacs, Katelin, and Sharmila Choudhury. “The Growing Gap in Life Expectancy by Income: Recent Evidence and Implications for the Social Security Retirement Age.” Congressional Research Service. May 2017.

Jackman, Tom. “Homicides Skyrocket across the U.S. During Pandemic.” Washington Post. November 21, 2020.

Johnson, Norman, Sarah Miller, and Laura Wherry. “Medicaid and Mortality: New Evidence from Linked Survey and Administrative Data.” NBER Working Paper 26081. November 2020.

Kaiser Family Foundation. “Marketplace Enrollment 2014-2020.” Accessed November 30, 2020.

Kaiser Family Foundation. “Status of State Medicaid Expansion Decisions.” Accessed November 30, 2020.

Keisler-Starkey, Katherine, and Lisa Bunch. “Health Insurance Coverage in the U.S.” U.S. Census Bureau. September 2020.

Maag, Elaine, Kevin Werner, and Laura Wheaton. “Expanding the EITC for Workers without Resident Children.” Urban Institute. May 2019.

Social Security Administration. 2020a. “Monthly Statistical Snapshot, October 2020.” Accessed November 30, 2020.

Social Security Administration. 2020b. “OASDI Trust Funds: 1957-2019.” Accessed November 30, 2020.

Tax Policy Center. "Key Elements of the U.S. Tax System." Accessed November 30, 2020.

U.S. Census Bureau. "Historical Income Tables: Income Inequality." Accessed November30, 2020.

Watson, Garrett. "How High are Other Nations’ Gas Taxes?" Tax Foundation. May 2019.